Economics

The good news on electricity prices

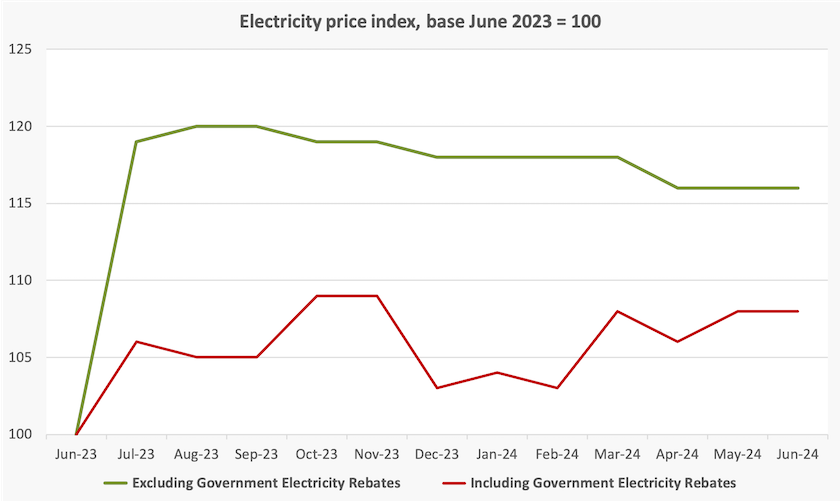

It almost passed unnoticed, a neat little chart in last week’s Monthly Consumer Price Index Indicator, reproduced below.

It shows, in the green line, how the electricity price would have moved but for the Energy Bill Relief Fund. The red line shows how those support measures have kept household prices in check. We are yet to see the effect of the 2024-25 extension of the EBRF.

Electricity prices shot up in 2023 because of huge fossil fuel price rises, explained by the Climate Council at the time.

But note what has been happening since – how that green line is slowly coming down, as we make the slow transition to renewable resources. That fall would be even steeper but for the costs incurred in electricity transmission, distribution and billing – all costs that have nothing to do with the mode of electricity generation. In fact the cost of transmission and distribution, capital-intensive industries, has been increasing because of higher interest rates.

This is not how the Coalition and the right-wing media are presenting the situation. We can expect to read stories about electricity bill shock, with the blame sheeted back to Labor for having irresponsibly put us on a path to renewables.

We have to read those stories carefully. If they have had the good sense to disconnect from gas, some people will be paying higher electricity bills, but without gas bills they will be paying less for household energy. For many in the eastern states it’s been a cold winter: even if the price of electricity has fallen, their bill may have risen if they used more. Partisan journalists often don’t distinguish between bills and prices.

Had the Abbott government not intervened to stop the transition to renewable energy, the shock of the 2022 fossil-fuel price rises would have resulted in a much more modest, perhaps unnoticeable, rise in electricity prices. We would have been many more years along the track to lower-cost renewable resources.

We can expect that wholesale price and therefore the retail price to go on falling as more renewable energy is rolled out. That is, if we don’t elect a Coalition government who will have to stop that rollout in order to justify the business case for building a high-cost nuclear “base load” system.

The economics of surfing

Surfing pumps $2.71 billion into the Australian economy and boosts wellbeing writes Ana Manero of the ANU, in her Conversation contribution summarizing research she has done on the economics of surfing.

She arrives at that $2.71 billion through the conventional economic techniques of considering the economic boost by those who spend directly on travel, accommodation, surfboards and so on. When she adds the multiplier effects of their spending she gets to economic benefits of $4.88 billion.

Such estimates, used to justify everything from the Olympic Games to local museums, are disputable, because people may have spendt that money on some other activity.

But less disputable are her estimates of the health benefits of surfing. She estimates the mental health benefits alone to be $5.6 billion a year, just from doing something difficult and challenging in a natural environment. She doesn’t start to calculate the benefits to physical heath from participating in such a demanding sport.

Surfers don’t have a powerful lobby, bullying governments into allocating scarce construction resources to building massive stadiums. They don’t demand that governments hand over precious urban green space, presently enjoyed by people engaged in active recreation, to be used by football clubs for training.

Apart from a few rough roads to remote beaches, surfing makes few calls on public resources. But without any economic justification governments keep pouring money into spectator sports that involve people sitting on their backsides in stadiums or watching big screens in pubs, when they could be out doing something physical.

The Reserve Bank’s alternative universe

Those who lived through the Cold War learned, long after the Soviet Union had collapsed, that there had been at least two occasions when military misjudgements could have set off a nuclear war of Mutually Assured Destruction.

Reading Gareth Hutchens’ report on the Reserve Bank’s decision to hold interest rates –Reserve Bank considered a rate hike in August meeting but left interest rates on hold –evokes a similar feeling. We have narrowly escaped MAD.

The Board’s statement on its decision carries no message about consideration of a rise in interest rates: that is drafted in the usual style of carefully-crafted ambiguity, with its usual conclusion: “The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome”.

Hutchens learned that the RBA had been considering raising the interest rate at the Governor’s post-meeting press conference. “She said a near-term cut in interest rates wasn't on the cards, and she wasn't expecting Australia to fall into recession at this point. She said the board only considered lifting rates, or keeping rates steady”. Because it is mentioned only in her press conference, and not in the board’s written statement, we are left to wonder if the idea of raising rates was Governor Bullock’s.

A near miss. We might ask if the RBA and the rest of Australia’s financial community are living in different worlds. Stephen Koukoulas, in Yahoo Finance – Great RBA misread risks Phillip Lowe-style interest rate mess: “Ignoring the screams” – writes:

It is fair to ask, what do the narrowly focussed, hugely specialised economists and analysts at the RBA know that agile and insightful global investors pumping hundreds of billions of dollars a day into the financial markets don’t know?

While the RBA has ruled out cutting rates over the next six months – one of its rare categorical statements – many analysts in the big banks believe that there will have to be a cut in interest rates before the end of the year. Peter Martin is one of the independent economists who believes that the RBA could be holding on too long: The RBA says don’t expect interest rate cuts for 6 months. Here’s why it could be sooner. (The Conversation)

The RBA Statement on Monetary Policy, which now comes out at the same time as the brief statement on the interest rate decision, carries the same message as the RBA’s shorter statement about inflation. It expects inflation as indicated by the CPI to fall in the short term, and then to rise again, as government measures to deal with cost-of-living pressures run their course. The Bank expects underlying inflation (as indicated by the “trimmed mean”), to fall only slowly, however.

The RBA has updated its short-term forecasts to predict that GDP and unemployment will be higher than previously forecast. That is counterintuitive, but it is consistent with the possibility of higher labour force participation and a more efficient allocation of labour. It is also consistent with its forecast that financial conditions will be more favourable for households than for businesses.

The overall impression one gets from the RBA’s analysis, however, is that if there are inflationary pressures in the economy, they are structural. That is, they result from a mismatch in demand and supply – a mismatch between the goods and services people want and need, and what the economy can provide. They do not result from some positive feedback loop of wages chasing prices, chasing wages, chasing prices in aself-perpetuating loop. Structural problems are best addressed by tax policies and by industry-specific structural adjustment policies, as were pursued by the Hawke-Keating government, not by the crude sledge hammer of monetary policy, which leads only to Mutually Assured Destruction.