Other economics

Supermarkets

The media have covered the government’s decision to make the Food and Grocery Code of Conduct mandatory. Subject to legislative approval, it is to accept all recommendations of a report into Craig Emerson’s review of the code.

There are to be penalties for non-compliance, and there is to be an anonymous channel to receive complaints about retribution and other breaches of the Code to protect suppliers who complain about supermarkets’ behaviour. Michelle Grattan has a short summary of the provisions in a Conversation article: Albanese government will impose mandatory code and big penalties to stop supermarkets treating suppliers badly.

This is one of the government’s initiatives dealing with the supermarket industry. As the ABC’s Georgia Roberts explains, although it may result in fairer terms for suppliers, it shouldn’t have any impact on consumer prices: supermarkets have plenty of capacity to absorb any extra costs associated with treating suppliers fairly. In any event, in the long run, consumers and producers can both benefit from a better-performing market.

The ACCC is conducting a separate enquiry into supermarkets’ pricing practices.

Another government intervention is the introduction of a quarterly survey of prices in Australian supermarkets, funded by the Commonwealth and conducted by the consumer group Choice. It published its first report last week. The results are striking. The price of a basket of standard goods is essentially the same in Coles and Woolworths shops, but is about 25 percent cheaper at Aldi.

Besides a short media release, Choice has a more detailed account of its research, including a description of its methodology, on its website. Or you can see Choice’s Ashley de Silva describe the findings in a short videoclip embedded in the New Daily report on the Code of Conduct.

Choice reports on regional variations. Prices in Tasmania and the Northern Territory are significantly higher than prices in other jurisdictions. In neither place is there any Aldi presence, lending weight to the proposition that the presence of another strong competitor helps discipline the market, but it is also relevant to note that Tasmania and the Northern Territory are both difficult markets to serve.

Based on a limited sample, they find that IGA was more expensive than the two major companies. At the other end of the spectrum they didn’t include Costco, which operates on a slightly different business model, a model that would almost certainly offer even lower prices than Aldi.

They also found that prices in Coles and Woolworths supermarkets in non-capital city locations are slightly lower than in capital cities. The price difference is immaterial, but it does not confirm the commonly-held belief that food prices are always higher in the country than in the cities.

Rather, it tends to confirm a general pattern that while food prices in large inland and coastal cities are much the same as in capital cities, prices in more remote locations are generally much higher. This phenomenon is not picked up in the Choice survey because large supermarkets are to be found only in reasonably-sized cities.

What is revealing is that many of the 15 non-capital city supermarkets they surveyed were probably enjoying a monopoly position. If they were exploiting that monopoly position we would expect, on average, that those supermarkets would be more expensive than those in capital cities, but this is not the case. This suggests that the presence of the other of the big pair in the same market does not result in lower prices.

That is counter to simple competition models, but it is in line with textbook theory on oligopoly pricing. That is not to suggest there is any collusion. The theory of oligopoly rests on the reasonably well-established idea that when there is only a small number of roughly equal-sized players in a market, no one benefits from starting a pricing arms race.

Recognition of this oligopoly structure is possibly the reason why many, including Allan Fels, writing in The Conversation, believe Emerson and the government should have gone further, and forced divestiture onto the industry. Fels notes that the Shop, Distributive and Allied Employees Association stood out as one party opposed to divestiture. Unions have less strength in a fragmented industry.

The reality of consumer behaviour: we don’t rationally assess our interests

Choice’s Ashley de Silva advises us not to shop on autopilot. It’s sound advice, but we are creatures of habit. We invest in learning how and where to shop, down to the placement of items on supermarket shelves.

It’s costly to shop around: economists and marketers alike recognize that consumers trade-off the benefits and costs of shopping around (“search costs” in economists’ jargon). That’s why we grudgingly fill up our car at the high-priced garages on the freeway rather than drive to the nearby town where prices are lower.

Accepting the gasoline price on the freeway is rational, because it’s a once-off transaction. In our regular shopping we spend, on average, about $200 a week, or $10 000 a year at one of the big two supermarkets.[1] There’s money on the table and most consumers aren’t picking it up.

The ABC business reporter Kate Ainsworth points out that the money has been on the table for a long time: the Choice inquiry isn’t telling us anything we didn’t already know. In her article If supermarket inquiries alone provided cost-of-living relief, groceries would already be cheaper at the check-out she is sceptical about the strength of comparative price information as a way to make consumers move. As the aphorism goes, you can take a horse to water but you cannot be sure it will drink.

The advertising industry would have us believe that it’s the power of advertising and gimmicks such as fly-buys that keep consumers attached to high-price businesses, but behavioural economists have a simpler explanation, backed with research. We just don’t take the effort to do a few simple calculations, particularly related to ongoing outlays or savings. We don’t calculate what we might save if we shifted to Aldi – perhaps as much as $2500 a year based on Choice’s calculations, and that’s every year! Or we are daunted by the upfront $130 membership fee for Costco, which would surely pay for itself within a month.

1. This is a back-of-the-envelope calculation. Coles and Woolworths annual sales total about $100 billion, and there are about 10 million households in Australia. That comes to $10 000 a year per household, or $200 a week. ↩

An inflation fright? Let’s cool down and look at the data

The general interpretation of the ABS Monthly Consumer Price Index Indicator for May is that inflation rose in April to 4.0 percent, which is higher than most economists expected. Any idea of an interest rate cut is gone: in fact a rise in rates is possible. The ABC’s Michael Janda provides an analysis along this line in his post “Nasty upside surprise” on inflation raises interest rate pressure on the Reserve Bank .

I don’t want to single out Janda: his approach is pretty well in line with most other professional economics journalists, but we should look carefully at the numbers in this, and other indicators of inflation, before making any categorical statements about inflation. Unfortunately the pressure on journalists to put something on media websites is such that few have time to look at the details in ABS publications of economic data.

In fact all the indicator tells us is that the index number rose by 4.0 percent between May 2023 and May 2024. That is, over a year, rather than in May 2024, as is the impression gained from reading journalists’ reports. In fact in May the index fell a little – from 123.7 to 123.6, and in seasonally-adjusted terms it showed no movement.

If this indicator were accurate enough we could conclude that CPI inflation has now fallen back to zero. Of course we shouldn’t make such a claim based on an incomplete indicator subject to significant margins of error when comparing two consecutive months, but there is strong evidence in the latest figures that inflation, as indicated by the CPI, has fallen sharply.

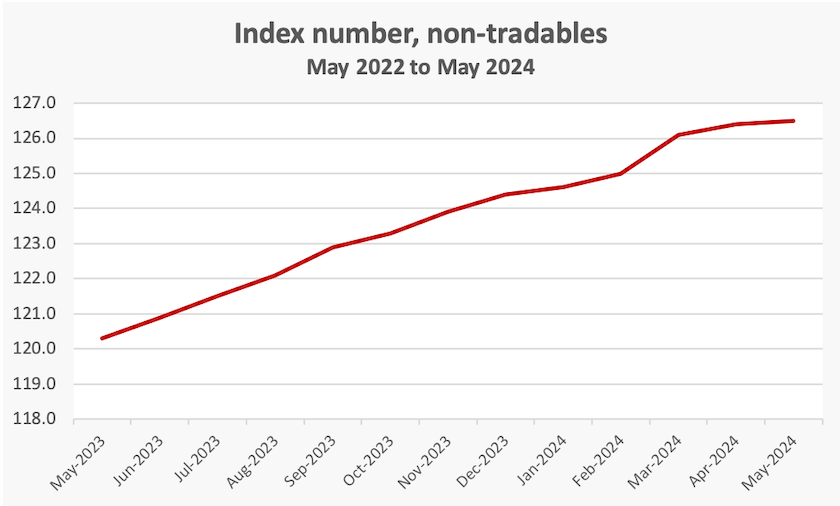

One of the most important aspects of CPI indicators is the distinction between “tradables” (i.e. traded on world markets), which are subject to the vicissitudes of world commodity markets, wars and exchange rates, and “non-tradables”, which are a reasonably sound indicator of the effect of domestic sources of inflation, particularly wages. The graph below shows how the “non-tradable” index number has moved over the year to May 24. There was a steep rise at the beginning of this year, but since then it has flattened out considerably.

That’s a warning against looking at the 12-month change in the indicator, and using that figure to say that inflation was X per cent in the latest month. That is simply wrong mathematically: Journalists’ habitual repetition of this flawed presentation doesn’t make it correct.

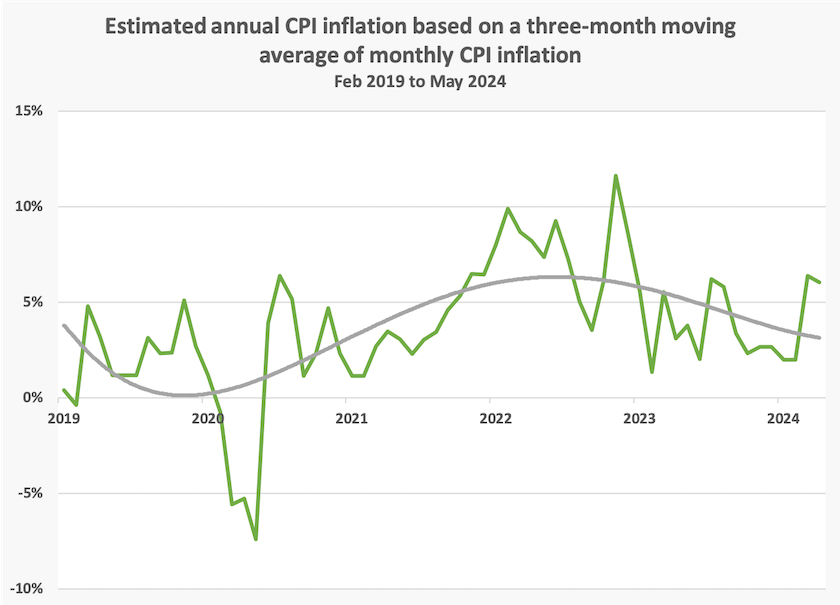

Because monetary policy works slowly, it’s useful to look at trends over a longer period than just one year.

The graph below is constructed from a three-month moving average of the CPI indicator. This smooths out much of the month-to-month sampling error, and therefore concludes with an indication of CPI rises in the last three months – March, April, May – leaving aside the data from the May 2023 to February 2024 period.

This moving average is shown below, along with a longer-term trend. There was indeed a small turn-around in the indicator, and the more important feature is the downward trend, from its high point in mid-2022 (just after the election).

The trend is in the right direction.

Stephen Koukoulas, writing in Yahoo Finance – RBA on cusp of major mistake for interest rates – makes the same point about trends . Monetary policy works its way through the economy slowly. He looks not only at the CPI, but also at employment, reminding readers that the RBA has the dual goals of low inflation and full employment. He points out that the unemployment rate has been on an upward trend since the start of last year.

That is, there are two trends – falling CPI inflation and rising unemployment – suggesting that the RBA should certainly not be raising interest rates. In fact Koukoulas suggests that it should now be cutting rates. Failing to lower rates is the “major mistake” to which he refers. To back up his warning he notes that in times past the RBA board has been much readier to lower rates when the economy showed signs of weak growth and rising unemployment.

Peter Martin is another commentator who believes the Reserve Bank is well on the way to suppressing inflation. He looks not only at published ABS trends, but also at reports from businesses, indicating that consumers have become more cautious in their spending, that firms are finding strong resistance to price rises, and that they are becoming less likely to offer wage rises. He wrote his Conversation contribution The good news is the Australian economy is about to turn up. Here’s why before the May indicator figure was released, but in it he noted the possibility of a 4.0 percent year-on-year rise in the indicator. But that was over the year, and economists were expecting prices to fall or stay steady in the month of May. As pointed out earlier on this post, the May indicator fell a little and was steady in seasonally-adjusted terms.

At the beginning of this post I mentioned Michael Janda’s initial response to the CPI indicator. Subsequently he has made another post “Bad mistake to set policy on one number”: RBA deputy plays down this week's inflation shock, in which he quuotes the RBA Deputy Governor’s reminder “It would be a bad mistake to set policy on the basis of one number”. This post has some insightful analysis of the Australian economy. I will link it again next week,