Economics

Inflation is coming down, but you wouldn’t believe it if you follow the media

On Tuesday the Reserve Bank will decide whether to raise interest rates. If it does it would be the twelfth rise in a little over a year.

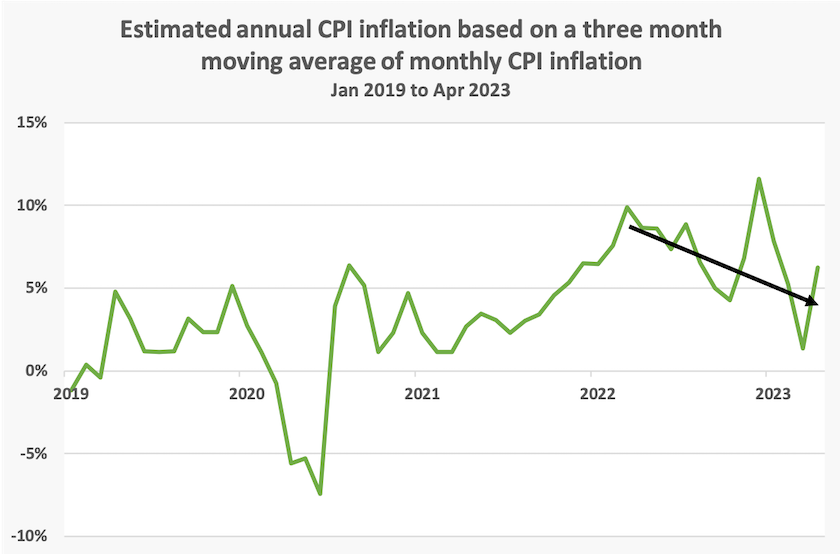

On Wednesday the ABS released its latest monthly CPI estimate. The general media interpretation is that because it shows annual inflation at 6.8 percent, up from 6.3 percent last month, the RBA will feel compelled to lift interest rates. But that’s based on a superficial reading of the ABS data: inflation is actually falling.

It is categorically wrong for anyone to assert that inflation is 6.8 percent. All we know is that between April 2022 and April 2023, the cost of a “basket” of goods and services (the CPI), representative of household consumption, rose by 6.8 percent.

That 6.8 percent is an estimate of past CPI inflation, incorporating data that is at least two months old and some that is 14 months old. It reveals little about what CPI inflation is now, which should be guiding the RBA. In any case, there is a greater margin of error in those monthly estimates than in the ABS’s more thorough quarterly estimates.

But many journalists who should know better are categorically stating that inflation is 6.8 percent, and are assuming that the RBA will increase rates in reaction to this headline figure, without any analysis or exercise of judgement.

This criticism of the presentation of inflation may come across as nitpicking, but it’s an important point when prices are volatile: what happened over the twelve months to April is only a rough guide to what’s happening now. In fact the trend in the CPI, drawn from these monthly estimates, suggests that CPI inflation probably peaked about a year ago and that the trend has been downward since then, as shown in the graph below.

If the Reserve Bank’s concern is the possibility of an outbreak of runaway inflation (what economists call accelerating inflation), these CPI figures give no suggestion of any such risk.

In fact, if we dig into the tables supplied by the ABS, we find that the month-to-month price rise in “All groups, seasonally adjusted”, is only 0.34 percent. That equates to only 4.1 percent annually.

Using another series reported by the ABS, the rise in “All groups excluding ‘volatile items’ and holiday travel”, we find that last month’s CPI rise has been only 0.17 percent, equating to 2.1 percent annually – well inside the RBA’s comfort zone.

OK, month-to-month movements have a high error of estimate, but the point is that there are many mathematically valid ways to interpret the current rate of CPI inflation. Perhaps the least defensible assertion is to say inflation is 6.8 percent.

In any event, in view of the nature of this latest spike, there is no evidence that raising interest rates would do anything to bring prices down. One of the most significant rises this month was in automotive fuel: 2.9 percent in one month. Also clothing prices have risen sharply.

Nothing in these figures suggests that CPI inflation is being driven by some wage-price spiral. As the Australia Institute points out, corporate profits provide a much stronger explanation of recent CPI rises. Price rises in gasoline, clothing and overseas holiday travel have little to do with Australian wages: they result either from higher margins in Australia or cost pressures in other countries. A rise in interest rates may have the effect of reducing demand-side pressures on prices (the basic economic model), but they would do nothing to bring down the prices of these imported goods.

Much of the discussion of the CPI has been about rent – possibly because the rent component of the CPI is separately identified in a scary-looking chart on the ABS statement. Monetary policy is probably the worst possible instrument in tackling rent, because for many property owners carrying mortgages, interest payments are a cost they can pass on to tenants. Higher interest rates tend to reduce housing supply, pushing rents up further.

The Reserve Bank is not some automaton that moves interest rates without exercising judgement. If it were, the entire board could be replaced by a computer generating an automatic press release each month. In fact the RBA employs some of Australia’s best economists. But it hides its talents under a bushel, particularly in its dumbed-down public statements.

If the RBA knows something that outside observers analysing published statistics don’t know, the RBA should reveal what has driven its judgements, rather than conveying the impression that it is relying on some simplistic Economics 1 model.

Also if it is so concerned about inflation, it should surely acknowledge that the only assured way in the medium to long term to have real (non-inflationary) wage growth is to address Australia’s poor productivity performance, which has fallen badly over nine years of Coalition governments. Every rise in interest rates suppresses those investments in the private and public sectors that can lift our productivity.

Is the RBA, in its obsession with the CPI – a short term indicator – thwarting its own objective of containing inflation?

The rental market – headline figures mask problems for renters in urban regions

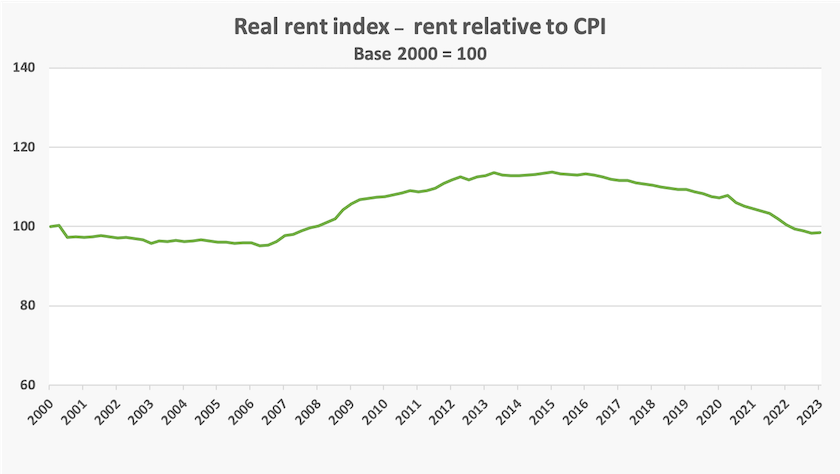

If you ask any reasonably well-informed person whether real rents – i.e. rents relative to the CPI – have fallen or risen, they will almost certainly answer that they have risen.

But as measured in the CPI, rents have been falling in real terms for the last eight years, as shown in the graph below.

That surely cannot be the case, in view of what we are hearing from welfare agencies, press reports, and people we know seeking rental accommodation.

Part of the explanation is that rents, as measured in the rental component in the CPI, have simply been keeping up with the CPI generally. Notice in the graph that for the last year or so the line has flattened.

The other explanation is that property owners tend to raise rents only when their properties become vacant. Only between a quarter and a third of rented properties become vacant in any one year. For the most part there is no rise in rents for established tenants, or if there are rent increases they are generally not too far from the CPI movement. Rents increase when properties become vacant, however: just in the last two years there has been a 20 percent jump in advertised rents for vacant properties.

This is one of the findings of a paper in the Reserve Bank Bulletin by Fred Hanmer and Michelle Marquardt, New Insights into the rental market. Their research reveals a great amount of detail about the rental market, particularly at a regional level.

They show that as the pandemic took hold, rents close to capital city CBDs (< 12.5 km) fell sharply, but as the pandemic has abated, rents in such regions have risen sharply, from the low pandemic base. But they’re still generally lower than they were before the pandemic. In part what we’re observing is a rapid return to normal conditions.

The authors report that the ABS is improving the data it collects to track rental prices as an important input into the CPI. But such data is based only on transactions that have occurred – actual payments based on successful tenancy agreements.

That means if you are sleeping in your car, or couch surfing because you cannot find or afford a rental property, your plight won’t be captured in the CPI. Writing in Eureka Street, Jennifer McVeigh, drawing on work by Anglicare, reports that women over the age of 55 are the fastest growing cohort of homeless people in Australia. Most of these women have never been homeless before. We need a great deal more informative data than can be captured in even the best-designed CPI.

Popular ideas about housing policy – mostly but not entirely in line with sound economics

The latest Essential Report includes three sets of questions on housing. A significant majority of respondents (69 percent) believe that there should be “further restrictions on foreign investment in residential property in Australia”, and 60 percent believe there should be “a freeze on rental increases”. Older respondents are strongly in favour of restrictions on foreign investment.

These responses should be of concern to policymakers. The success or otherwise of build-to-rent projects is dependent, in large part, on relaxing some present restrictions on foreign investment. Support for rent freezes is understandable, but rent freezes, except when applied for a very short period such as during the worst of the pandemic, have many unintended consequences. Also when there are rumours of rent freezes, unscrupulous property owners raise their rents in anticipation and can make a windfall in a property market where supply is constrained because of rent freezes.

Responses to other questions in the Essential survey tend find an alignment of public attitudes and good public policy.

One statement Essential has put to respondents is “Prevent wealthy families from using family trusts to split their assets to minimise tax”, seeking their agreement or otherwise. This is not specific to housing: rather it is about the distributive justice of our entire tax system.

That statement gained 57 percent support, and even 50 percent of Coalition voters were in favour of action on family trusts. Over many years Labor in opposition has promised to crack down on family trusts, but in office it seems to have forgotten this important tax reform.

Perhaps the next Essential survey could ask respondents what they think of the advice of the RBA Governor that people should share their rentals. In the same spirit it could ask people’s view on concessional registration fees for people who sleep in their cars, or provision of blankets from army surplus for people sleeping rough. Such questions would be appropriate in a country that has given up and is resigned to a perpetual housing shortage. Surely we haven’t sunk to that level.

A spike in electricity prices is coming

Last week the Australian Energy Regulator issued the default market offer electricity prices for 2023-24 for Queensland, New South Wales and South Australia. (The other National Electricity Market states, Victoria and Tasmania, are under different arrangements, but their price rises will be broadly in line with the AER’s.)

These price rises, between 20 and 25 percent in nominal terms, take effect on July 1. They effectively determine the maximum price consumers can be charged. You can plod your way through the AER determination (linked above), or listen to Clare Savage, Chair of the AER, explain the decision in an 8-minute session on ABC Breakfast: Energy Regulator releases ceiling price for NSW, SA and Qld.

She explains that these rises are much lower that the AER feared would occur, before the Commonwealth intervened in the coal and gas market. Last October they were looking at rises of 35 to 50 percent.

She also explains that many people are eligible for a $500 rebate on their bills, funded jointly by the Commonwealth and the states. That should more than offset the rise in their bills for most customers eligible for these rebates.

The price rises relate mainly to the cost of fossil fuels, and to problems in Australia’s old coal-fired generators. They also apply along the line to electricity transmission and distribution (“poles and wires”) and to “retailers” – the commission agents at the end of the supply chain.

Privatized and costly

Much of what we pay for electricity – at least 60 percent – has nothing to do with the cost of generating electricity. Rather it is for these transmission, distribution and retail entities, which came into existence when the state electricity utilities were broken up and privatized. The transmission and distribution firms, as monopolies, are subject to absurdly generous price regulation, and the retailers, while subject to competition, are a whole new layer of overheads which weren’t necessary when the state-owned utilities controlled the supply chain.

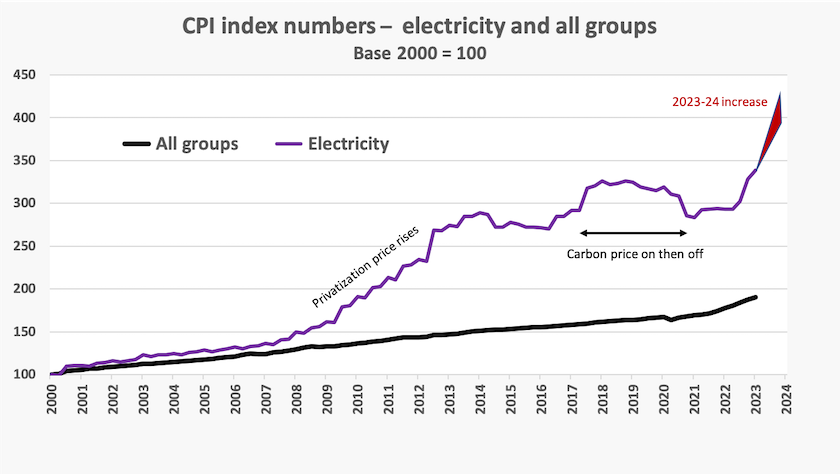

The graph below shows the CPI index numbers for electricity over this century so far, compared with the “all groups” CPI (i.e. the commonly-used indicator of household inflation). It’s been a hard time for households, particularly those lacking the means or initiative to reduce electricity consumption.

For many years, going back to 1980, electricity prices more or less tracked the CPI. To an extent that was unsustainable, because the state-owned utilities were not retaining enough surplus to allow for necessary system expansion and replacement of ageing assets. But the main increase came from privatization, with all its inefficiencies and extra costs – higher profits, higher managerial salaries, advertising, and transaction costs of a broken-up supply chain. Then there was the short-lived carbon price – notably less significant than price rises associated with privatization. Finally there have been price rises associated with Russia’s invasion of Ukraine, and our permissive treatment of gas companies.

The general advice offered to consumers is to shop around for the best deal. As Lurion De Mellow of Macquarie University writes in The Conversation, that’s not as easy as it should be. Even he, a lecturer in energy economics, finds the comparison websites confusing. It is hard to find like-for-like comparisons.

Scott Adams in his Dilbert comic strip invented the term “confusopoly” as a description of “a group of companies with similar products who intentionally confuse customers instead of competing on price”. Josh Gans, of the University of Melbourne, recognized the academic validity of confusopoly, and found it fitted perfectly into theories of behavioural economics: his lecture slides are on the ACCC website.

Even if some people can navigate their way around websites, because of the way markets work and the way they are regulated, all that happens is that they get good deals while others pay higher prices, because the process is zero-sum. Only those who have time on their hands, and some analytical ability, will get the good deals. In the end all that happens is that retired engineers who have some mastery of Excel are subsidized by the busy and by those who didn’t pay attention in their high-school math classes. It’s hardly a fair or efficient outcome.

The better consumer response is to use less electricity from the grid, particularly at times when it is expensive, and to generate and store some of their own. Saul Griffith’s Quarterly Essay The wires that bind goes through the engineering and arithmetic of DIY energy efficiency. Insulating walls, installing heat pumps, throwing out gas appliances, double glazing, installing panels and batteries, are all ways to cut electricity bills. Most investments are, or should be, no-brainers, with such good returns that one could finance them at credit card interest rates and still be ahead. The best aspect of such investments is that not only do they save you money, but in terms of reducing demand, particularly for electricity at peak time, they also make electricity cheaper for everyone, while saving the planet.

Of course there are renters, or those who live in the worst locations such as a middle floor of an old and poorly-built apartment block, or who live in the shadow of Hobart’s Mount Wellington, who have little opportunity to improve their energy efficiency. That’s where building standards should apply, and as explained in the Conversation article Here’s how to ensure renters can cash-in on rooftop solar by three ANU experts, there are ways governments, through regulation and education, can provide incentives for property owners to improve the energy efficiency of their buildings, to their own and their tenants’ benefit.

Exploit vulnerable consumers now, regulate later

“Buy now pay later” came to Australia in 2017. It is only now, six years later, that the government has decided to recognize BNPL as a credit product, and to regulate it accordingly. On ABC Breakfast last week Financial Services Minister Stephen Jones said that “if it looks like a duck, walks like a duck, and sounds like a duck, it’s probably a duck, and I think it’s about time that we regulated them as credit products and put the right sort of consumer protection provisions in place, bringing them inside the national Consumer Credit Act”: Buy now, pay later, to be regulated.

We are probably familiar with BNPL on the consumer side: it’s almost impossible to buy anything small on line without seeing the option of four easy fortnightly payments. We may be less aware that BNPL makes most of its profits from merchant fees.

In a 2021 Reserve Bank Bulletin paper – Developments in the Buy Now, Pay Later market -- Chay Fisher, Cara Holland and Tim West describe the industry’s business model. While merchant service fees are around 0.5 percent for debit cards, 1.0 percent for credit cards, and 2.5 percent for Paypal, they are around 3.0 to 3.9 percent for BNPL. In an interview on ABC Drive last week Andrew Grant of the University of Sydney Business School says merchant fees are now around 5 percent: Buy now, pay later services to be regulated under credit laws.

Under agreements with the BNPL providers, merchants are not permitted to charge a service fee, which really means that they cannot offer a discount for those who don’t use BNPL. In other words, we all finance BNPL, through what is in effect a privatized sales tax.

According to Grant, about 25 percent of Australians have a BNPL account. A short article by the banking platform Frollo – The rise of invisible debt – reveals that BNPL has been particularly popular with Gen Z – people now in their twenties. Almost a quarter of BNPL users pay off BNPL with credit cards. That is, those who are able to get a credit card. The same article reveals that while BNPL is used by Gen Z, only 12 percent of Gen Z use a credit card to pay off BNPL. That is consistent with Grant’s suggestion that BNPL is the resort for those who cannot get a credit card.

Perhaps when there were only two BNPL providers – Afterpay and Zip Co – no one could get into much trouble, but with many more firms in the market, all offering easy credit, people can run up multiple debts: Grant mentions that about 10 percent of Australians have more than one BNPL account. In the interview with Stephen Jones, Peter Martin mentions a person who has 8 BNPL debts.

Writing in The Saturday Paper – Afterpay and our addiction to debt – John Hewson puts BNPL into a wider perspective. He is surprised that it has taken so long for the government to regulate BNPL. That was “a task conspicuously neglected by the previous Coalition government”. He urges the Albanese government to be more supportive of a current parliamentary review of the Australian Securities and Investment Commission.

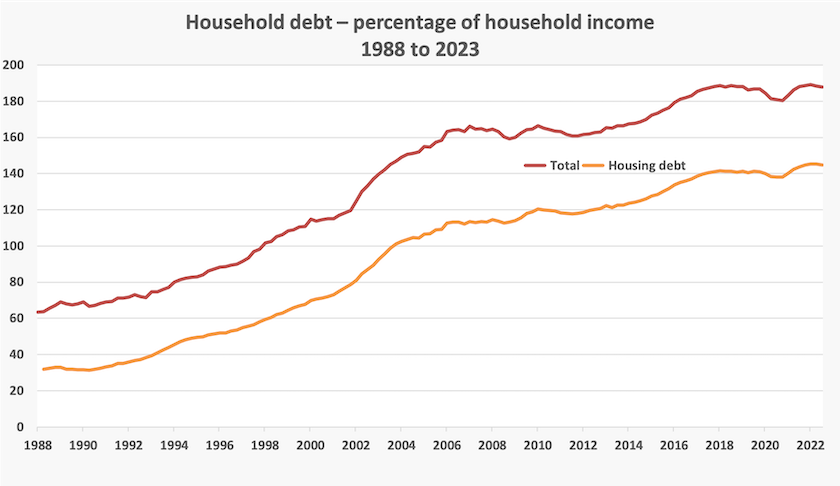

He also adds his voice to the concern about household debt, which as a percentage of income, has been rising for many years. In 1988 it took about 7 months of income to pay off the average household debt: now it takes 22 months.

Maybe, as Hewson hints, we don’t have an appetite for delayed gratification. But maybe there is something wrong in a society where a sizeable proportion of people, perhaps a quarter, are so cash poor that they feel they have to obtain six weeks’ credit for small purchases.

Sports betting

In a rare but welcome expression of concern for the most financially vulnerable in the community, Opposition Leader Peter Dutton has called for restrictions on sports gambling.

The Alliance for Gambling Reform notes that pressure for gambling reform seems to be coming from the Coalition, even though “the areas where gambling hits hardest, particularly poker machines, are the poorer, heartland suburbs of the Australian Labor Party”. The Alliance’s post Labor’s gambling ties holding back proper reform lists a number of areas, particularly in state politics, where the Coalition seems to be ahead of Labor with policies that would reform gambling.

The Alliance for Gambling Reform has expressed support for a bill by federal MP Zoe Daniel proposing a ban on gambling advertising on TV, radio and streaming services. The Alliance also calls for a prohibition of gambling with credit cards and other forms of “buy now pay later” schemes. There is a Parliamentary committee inquiry into online gambling, which should be reporting later in the year.

The latest Essential Report finds that only 16 percent of respondents believe that sports betting should be allowed at all times, even during events, while 43 percent believe sports betting should be banned altogether. Women, Labor supporters, and older people have more negative attitudes to sports betting than Coalition supporters, men and younger people.

It's hard to see what is holding back our state and Commonwealth Labor governments from gambling reform.

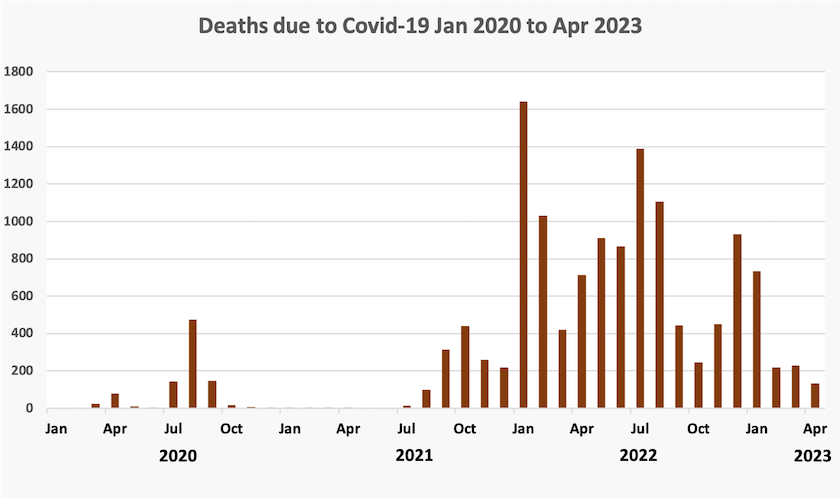

Covid-19 deaths – a summary

From the time Covid-19 broke out in early 2020 to April this year 17 198 Australians have died of or with it.

The ABS has gathered state and territory data and published a statement COVID-19 Mortality in Australia: Deaths registered until 30 April 2023, covering mainly the 80 percent of those deaths (13 718) where Covid-19 has been the underlying cause of death.

Their findings can be summarized in two charts.

First, the incidence of deaths over those 40 months:

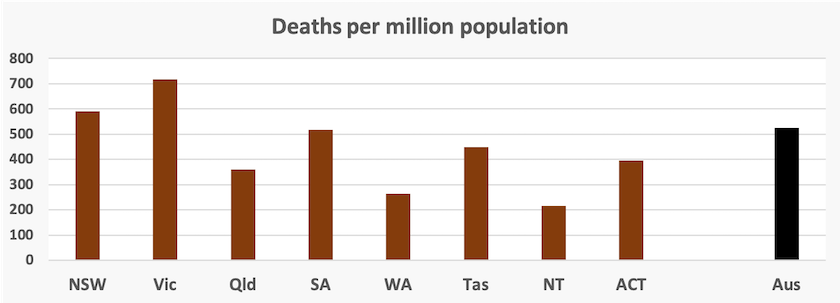

And second, deaths by state and territory:

The ABS provides a breakdown by sex and age: 88 percent of deaths caused by Covid-19 have been among people aged 70 or older.

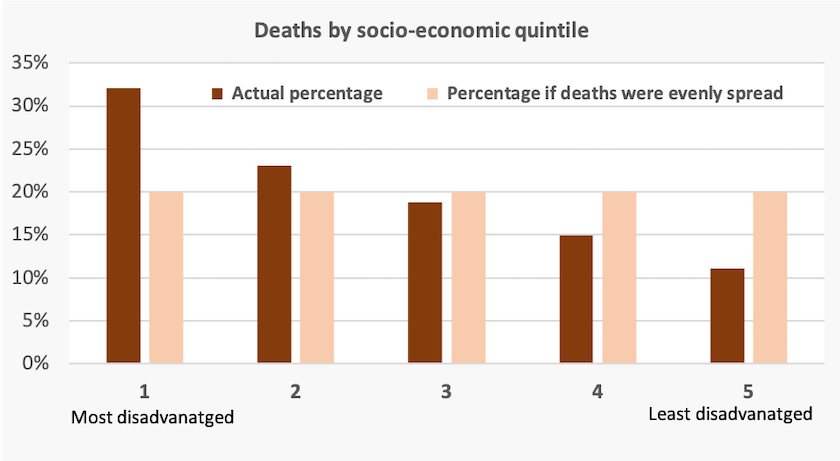

Another chart derived from the ABS statistics shows deaths by socio-economic quintile:

The ABS data goes up to April. Data from the Department of Health indicates that Covid-19 deaths in May have been rising, but if there is a winter spike it should be much lower than the December-January spike.