Economics

Immigration – shifting policy and cleaning up a mess

In her address to the Press Club on Thursday Minister Clare O’Neil said our migration system is “unaligned with Australian values”.

That is a reference to an established but unannounced policy of successive Coalition governments to use immigration as a means to suppress wages, particularly in low-skill occupations. One consequence has been the presence in Australia 1.8 million people on short-term visas, many of whom are in conditions best described as indentured labour, where conditions of minimum wages and workers’ rights don’t effectively apply.

The government’s policy is directed at re-establishing permanent residence as the main feature of immigration. The emphasis will be on bringing into Australia people with needed skills who can work in well-paid occupations.

The government is also cleaning up an administrative mess. “Our system is slow and crazily complex” said Minister O‘Neil. It lets down every stakeholder – prospective immigrants, employers, and the community generally. In many aspects it fails any reasonable test of fairness.

Details of the changes are in a 190-page document unpretentiously named Review of the migration system. It’s a draft, subject to a consultation process described on Home Affairs website. But O’Neil’s speech makes it clear that its principles and main provisions are now government policy.

The government seems to have the unions and peak business lobbies on side as revealed in a 16-minute discussion on ABC Breakfast on Friday, with Michele O’Neal of the ACTU and Innes Willox of the Australian Industry Group. The only minor tension is between corporations’ interest in filling skilled jobs quickly and unions interest is finding opportunities for Australian-trained workers., but the general agreement is that a skilled and therefore well-paid workforce would be good for all stakeholders, and after years of neglect it will take time to boost our own capacity for skills training.

While business and unions may be onside, there is understandable community concern about the stress a higher rate of permanent rate of immigration will place on housing and infrastructure. The numbers being bandied around suggest that as a proportion f our population anything being considered is well short of the postwar immigration boom 75 years ago.[1] That is not to downplay the problem however: housing is a difficult economic and political problem.

Provided resources are available there should be nothing to stop the government from borrowing for housing and infrastructure. That is borrowing for investment, which would strengthen the public balance sheet. That net debt can be repaid by well-paid immigrants and other workers.

If the government manages to crack down on exploitation of immigrants and bring their wages up to acceptable levels, there may be some rise in the price of our vegetables, hotel rooms, meals out and other products of industries with a concentration of low-skilled immigrants. That may show up on the CPI as “inflation”, but it should more properly be seen as a restoration of normal price levels.

1. The figure being bandied around is that net migration could be somewhere in excess of the 235 000 included in the budget. That suggests a rate of around 1.0 percent of our population of 26 million, to take a high estimate. In the 1945 to 1955 period we were bringing in about 100 000 migrants a year, on a population of 8 million, suggesting a rate of 1.3 percent. That was also a period of strong family formation among native Australians. We coped, but then as now there were housing shortages. ↩

The Reserve Bank Review – keep the cash target but change the Bank’s governance

Even if the government were to implement all 51 recommendations of the Review of the Reserve Bank before next Tuesday’s meeting, it is doubtful if there would be anything different in the Bank’s decision whether to lift or hold the cash rate. The Bank will be guided by the CPI for the March quarter as evidence of inflation and the March quarter Labour Force data, which showed unemployment steady at 3.5 percent.

Had the review’s recommendations been implemented before the Covid-19 pandemic, the Bank may have been more cautious in its moves: between April 2019, when the pandemic broke out, and November 2020 it pushed the cash rate down from 1.50 percent to 0.10 percent, and that sent the real rate into negative territory, even though there was already plenty of money sloshing around the world. Under the governance arrangements recommended in the report it would almost certainly not have made the implicit promise that rates would be frozen until 2024.

The review points out that the RBA has had huge difficulty in getting CPI inflation into its two to three percent target range. With all the current talk of high inflation it’s hard to remember that until quite recently inflation was below the two to three percent range.

In that regard the review cites the views of economists who believe that it was mistaken in holding the cash rate at 1.50 percent from 2016 to 2019: it should have reduced interest rates until inflation rose to its comfort zone. According to conventional theory a looser monetary policy would have resulted in a lower rate of unemployment.

But we should note that over this period the real interest rate was hovering around zero. Low-cost money wasn’t doing much to stimulate business investment, and in Australia the Coalition government, constrained by its “small government” dogma, missed the opportunity to invest in public assets. There was plenty of liquidity in the world, but all it was doing was to contribute to asset-price inflation, particularly housing. That is part of a wider story about the collapse of neoliberalism, well beyond the scope of the Reserve Bank review. The review doesn’t step into such heretical territory.

Anyone looking through the review for a higher inflation target will be disappointed: Recommendation 2.1 – “there should be a flexible inflation target of 2-3 per cent” – makes it clear that there should be no change. But the review hints that the RBA doesn’t have to attack inflation like a bull at a gate. In what can be read as a rebuke of the RBA’s ten rises in ten months, it states, as an example of how that objective may be realized:

… if inflation is above target and employment below target following a supply disruption, the RBA can seek to return inflation to target more gradually than otherwise to achieve better employment outcomes. Equal consideration should be given to price stability and full employment in making such judgements.”

One of the more important suggestions, largely missed by the media, is Recommendation 3.2:

The RBA and Treasury should develop an Australian Macroeconomic Policy Research Program to promote applied research and analytics on Australian monetary, fiscal and financial policy, working with universities and think tanks that have such programs.

This and related recommendations acknowledge that the workings of macroeconomic and fiscal policy are not settled as robust theories. Peter Martin, in an interview on the ABC –Review addresses cultural and structural problems at the Reserve Bank – suggests that central banks around the world, who have been manipulating the levers of monetary policy and seeing inflation respond in line with the models, may have just gotten lucky until recently. They may have been actors in a global post hoc ergo propter hoc fallacy.

Reading the report’s accounts of undershoot and overshoot, and of the bank moving too slowly and too quickly, one is left with the impression that monetary authorities do not have a grasp of the dynamics of monetary policy. They don’t seem to realize that they are intervening in a complex physical and social system with time lags, feedback loops and tipping points. The Phillips Curve, a standard economist’s model used to guide monetary policy, presents a simple mathematical relationship between unemployment and inflation, as if both are unidimensional entities that need no disaggregation, and as if the relationship is causal, frictionless and instantaneous.

In that same 12-minute ABC interview Martin discusses the two governance and management issues that are central to the review.

One is about the need for a separate expert monetary policy board, with an emphasis on the word “expert”. The board most suited to the organization’s banking functions is not the board most suited to the conceptually far more difficult task of setting monetary policy.

The other is about the management culture in the bank. It seems to have been an organization entirely focussed on the CEO – in this case the chairperson. The staff’s job was to provide secretariat services for the board, and the board’s job was to legitimize the chairperson’s proposals.

Such a culture is inimical to dissent or even questioning. Chapter 4 of the review – “an open and dynamic RBA” – finds that the RBA “has a hierarchical culture, with a lack of or inconsistent delegation and an aversion to risk taking. This has resulted in some staff members feeling disempowered”. The RBA recruits some of the country’s best graduates in economics, but it does not use them well.

Regarding the board, its recommendations are mainly about more public exposure, and accountability. It also wants the board members to be able to draw on the expertise of the bank’s staff, in contrast to the present arrangement where all advice is mediated through the chair. It is hardly surprising that the review warns of the risk of groupthink.

In its criticism of the RBA’s hierarchical culture, with its focus on the top executive, the review notes that in this regard it is “like many public sector agencies”. Its recommendations for reform of the RBA could well apply to all public sector agencies where tight control of the CEO’s agenda comes at the expense of productivity and responsiveness to the public’s needs.

Writing in The Conversation Isaac Gross of Monash University gives a broad summary of the review, and of Treasurer Chalmers’ initial response: Reserve Bank revolution: how Jim Chalmers will recraft the RBA for the 21st century. He confirms Peter Martin’s report that during the pandemic the staff explicitly recommended against forecasting how long interest rates would remain at very low levels, and that this misgiving was never communicated to the board.

If the government implements the review’s recommendations, including those designed to create a board of experts rather than of the government’s ideological mates, the mistakes of the last ten years may have been avoided. But it is disappointing that the review seems to treat “inflation” as a well-defined and clearly measured phenomenon.

For policymakers it’s troublesome that the word “inflation” describes both the circular and self-sustaining phenomenon of prices and costs following each other, and the way, in response to a major development in the economy, there is usually a once-off adjustment in prices. The former is the runaway inflation observed in the Weimar Republic, or the inflation staved off when the Hawke-Keating government used the Prices and Income Accord to break the cycle of wages pushing up prices, which pushed up wages and so on, in a metastable feedback loop. The latter is a once-off reaction to, for example, the shock of a war, or the election of a government determined to protect minimum-pay workers from exploitation, resulting in price rises for broccoli, cafe latte, and hotel rooms.

An earlier example of such a shock was the introduction of the GST in 2000, when there was a once-off boost in the CPI, which was followed by a rise in the interest rate, even though there was no indication of the economy overheating.

This difference between these two forms of inflation is not adequately covered in the conventional textbook distinction between “cost push” and “demand pull” inflation.

Another problem is that the RBA seems to rely on the CPI as a measure of inflation. Technically it is only an indicator of movements in households’ cost-of-living: there are other inflation indicators. That may not matter much because all indicators seem to converge over time. What matters more significantly is that the CPI ignores the biggest component of housing costs – the price paid for land. Technically that’s because land is an item of capital that is not consumed: it’s therefore out of place in a consumer price index.

That distinction doesn’t make much sense to the person who is just as inconvenienced by the rising cost of housing as with the rising cost of gasoline or bread. In any case the distinction between “capital” and “consumer” goods is not a clear one. Economists regard land as a fixed capital asset, but through planning decisions, including the provision of infrastructure, governments can produce land suitable for building houses. Conversely, as we have seen with closure of railroads, and flooding, land can lose its real value rather quickly. We should be careful in allowing rules of classification to determine public policy.

The government under pressure from all directions to increase Jobseeker payments

It is hardly surprising that in the pre-budget period the government should receive a letter on ACOSS letterhead putting the case for an increase in social security payments.

What is striking about the open letter to the prime minister calling for the government “to substantially increase JobSeeker, Youth Allowance and related income support payments” is the range of signatories on the letter.

These are not just the usual suspects in welfare movements. Among federal politicians only One Nation and the National Party are missing. There are independent economists, former senior public servants, and prominent individuals without any partisan connection. Ken Henry has written in The Guardian that Forcing the most disadvantaged to live on $50 a day is cruel.

In last week’s roundup there was a link to the Report of the Economic Inclusion Advisory Committee, which presented the case for lifting Jobseeker payments, and there were links to the economic case for increasing Jobseeker. This open letter goes beyond those economic arguments: it presents the moral case for increasing social security payments: “We cannot leave people with the least behind.”

In relation to Jobseeker, Danielle Woods of the Grattan Institute has written about the three myths that keep Australians in poverty, basically dispelling the idea that the unemployed are slackers. The first myth is that the typical Jobseeker recipient is a “work-shy twenty-something playing video games in their parents’ basement”. In fact they’re typically over 45, female, and many are people who have been pushed off disability support and other payments in recent years. The second myth is that it’s easy to find a job, but as she points out it isn’t. The third is that unemployment payments need to be low to give an incentive to find work, but even if Jobseeker were increased to the level sought by the Economic Inclusion Advisory Committee there would still be a strong enough financial incentive to find work.

The case for program evaluation

CEDA (The Committee for Economic Development of Australia), has released the third instalment of its Disrupting Disadvantage series, a project started in 2019 that “seeks to identify areas where disadvantage might be disrupted, and to use this as a starting point for a more systematic approach to addressing the problem”.

The project aims to achieve better outcomes from Commonwealth and state government programs directed to reducing poverty. In spite of rising expenditure on such programs, income poverty remains stubbornly high.

Many programs are introduced without a clear definition of what “success” should look like, and without any process of evaluation. (Public policy texts stress that an evaluation mechanism should accompany program design.)

In its summary CEDA writes:

What is holding back change is a complex system that encourages policymakers to implement rapid responses to societal problems, rather than insisting on regular, proactive evaluation of existing programs. This is compounded by challenges in undertaking evaluations and a lack of resourcing, leading to long-term atrophy of evaluation culture and capability.

It notes that the Albanese government has stated a commitment to establish an office of Evaluator-General. That is a good starting point. There should be a systematic evaluation of all programs and the government “must invest in developing data assets and data availability and upskilling public servants to improve capacity and capability”.

We miss a heap of opportunities to collect and assemble data. You can hear CEDA’s Cassandra Winzar in a 2-minute YouTube clip explaining how effective capture and evaluation of data can improve program effectiveness.

It’s an important project, because in “developed” countries social security programs, generally involving large transfer payments such as age pensions, disability support and support for the unemployed, have tended to crowd out other government expenditure on education, research, health care, public health, protection of natural resources, and infrastructure – programs that contribute to a nation’s enduring prosperity and which, if well-designed, reduce the need for distributive welfare payments.

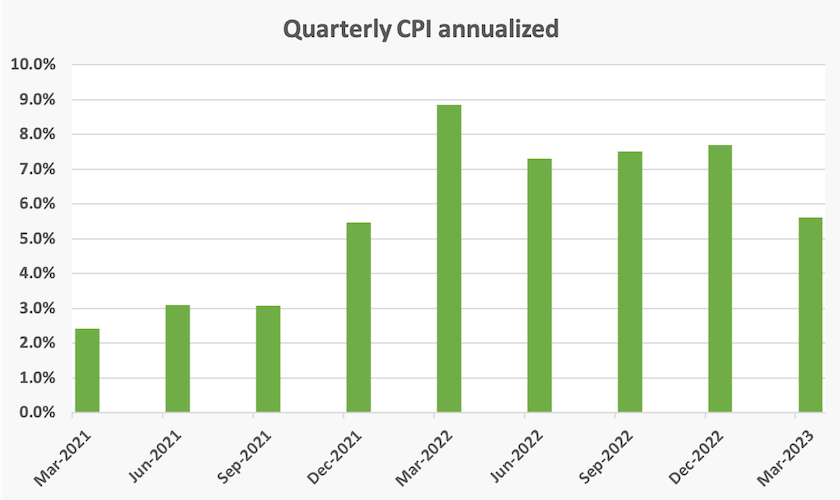

The March quarter CPI – what does it tell us?

Inflation is 7.0 percent. That’s what the ABS Consumer Price Index, released on Wednesday, tells us.

Or does it?

That figure is a pretty good indicator of how the average household’s cost-of-living has gone up over the 12 months to March. It’s probably overstated somewhat because of what statisticians call the “substitution effect”.[2]

But what does the ABS tell us about how inflation is tracking? That 7.0 percent is a comparison of prices in the March quarter 2022 with prices in the March quarter this year. But if the Reserve Bank is doing its job it wants to know where inflation is heading, not where it has been. It wants to know if inflation is a serious problem, and whether monetary policy can do anything useful to arrest it.

The ABS reports on far more than one headline figure covering a year. It also gives some quarter-to-quarter and even month-to-month data.

The rise in the most recent quarter, March, was 1.4 percent. Annualized that’s 5.7 percent. The trimmed mean, which excludes some extraordinary changes, is 1.2 percent – an annual rate of 4.9 percent.

Then there’s the ABS Monthly Consumer Price Indicator, released on the same day. It tracks the prices of a smaller basket of goods than the CPI. It looks at price movements only from February to March, which makes it more current than the CPI, but it is subject to a higher sampling error than the CPI. It shows a monthly rise of 0.6 percent, which comes to an annualized figure of 7.4 percent, but this series is very noisy. Its trend is certainly downwards, however.

To get some idea of where headline inflation is headed it’s also informative to look at what’s been happening over the last couple of years, as we have emerged from the Covid-19 recession. Eyeballing a graph of annualized inflation, as indicated by quarterly movements, suggests inflation peaked quickly and is now slowly on the way down. Such overshoot and correction are not uncommon in economies recovering from a recession.

When one considers the nature of recent price rises, a detailed consideration of the CPI suggests that raising interest rates may not do much to rein in inflation. Of the ABS’s eleven major categories of expenditure, the highest price rises have been in health and education, two items for which demand is comparatively inelastic. If the bank reduces people’s spending power by raising rates, they will still be spending on health and education.

Also disaggregated CPI data shows that rental prices have been a significant contributor to inflation over the last two years. If higher interest rates suppress investment in housing, the medium to long-term effect of higher interest rates would be to decrease housing supply and therefore to increase rental prices. Monetary policy is not only a crude tool; in cases it is counterproductive.

On housing the same CPI bulletin has a link to a research report, prepared by ABS staff, New insights into the rental market, that goes into a great amount of detail, including geographical detail, about the rental market. It confirms that although over the last few years rents rose faster in non-metropolitan regions than in the capitals, more recently rents in capital cities, particularly in regions close to the CBD, have shot up quickly. It also reveals that rent increases are higher when there is a change in tenant than when there is a continuing relationship. It is understandable that the Greens are calling for a mandated freeze on rents, but rent freezes are the textbook example of well-intentioned policies with horrible unintended consequences.

2. From quarter-to-quarter the CPI is based on a fixed basket of goods and services, but if some prices move faster than others, consumers may compensate by substituting items. For example, in the March quarter, because of unusually wet weather, potato prices rose strongly, but rice is an alternative source of carbohydrate. An economist friend has reminded me that recently the price of milk has risen much faster than the price of beer: to what extent are they substitutes? ↩

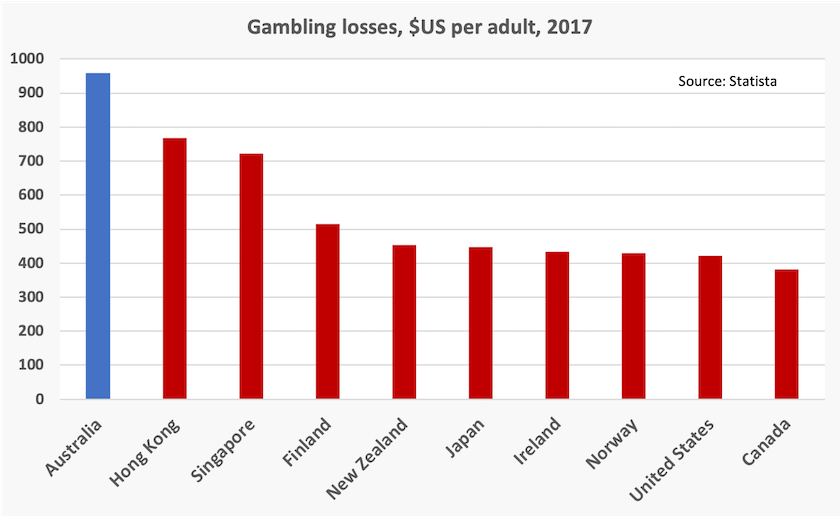

Australians lose around $25 billion a year in legalized forms of gambling

Stop to think about that $25 billion. It’s $1 000 for every Australian – children and adults. Or $2 500 a household. These are average figures, and we know that half or more Australians either do not gamble at all, or if they do it’s only incidental expenditure (Two up on Anzac Day perhaps). Losses in households with problem gamblers are in the order of tens of thousands.

The Australian Institute of Family Studies has produced two short research snapshots of gambling in Australia.

Gambling participation and experience of harm in Australia is about the distribution of gambling behaviour. Young people aged 18-34 are most likely to be classified as “being at risk of gambling harm”: 71 percent of young men and 55 percent of young women who gamble are so classified.

It also finds that our attitudes to gambling are generally libertarian, but most of us believe gambling should be discouraged and that there are too many opportunities for gambling.

Community attitudes towards sports and race betting advertising in Australia confirms that most Australians believe that there is too much sports and race betting. People believe that sport betting should be more strongly regulated and sport clubs should not have commercial relationships with betting companies.

These are summarized in a shorter AIFS post: Gambling participation, experience of harm and community views.

The ABC’s Mark Rigby pulls together the AIFS findings, with a focus on sports betting: Young gamblers losing more as social media presence of sports betting agencies grows. He points out that per capita Australia has the world’s highest level of online gambling expenditure.

This is in line with data on all forms of gambling, where Australia holds first place, as shown in the chart below. That chart probably understates the extent of our lead over other countries, because much of the gambling in Hong Kong and Singapore would be by visitors from other countries.

Another recent contribution on gambling is from the ABC’s sports journalist Jack Snape, who reports on the hearings of the Parliamentary inquiry into online gambling and its impact on those experiencing gambling harm. Snape’s article – Betting inquiry sees wagering companies squirm over blocking winning gamblers – portrays an industry with a business model designed to exclude well-informed gamblers, leaving only the naïve who are unable to incorporate the mathematics of probability into their reasoning. He also reports on the pathetic rationalizations the industry’s spokespeople have been presenting to the inquiry.

Just this week the government announced a minor reform in its intention to ban the use of credit cards in online gambling. But there is a long way to go: the govenments of New South Wales, Queensland, Victoria, the ACT and the Northern Territory – all Labor – seem to lack the gumption to take on the poker machine lobby.

As some foreign observers comment, gambling in Australia occupies the place of guns in America.

If you want a good job, change your name to John or Jill Smith

The journal The Leadership Quarterly reports on a study that reveals significant bias against people from ethnic minorities applying for “leadership” positions.[3]

Such studies have often been undertaken in the US, but this one – Is there a glass ceiling for ethnic minorities to enter leadership positions? Evidence from a field experiment with over 12,000 job applications – was conducted among Australian firms, and the results are disturbing.

The experiment involved sending out 12 000 applications for 4 000 positions, a controlled proportion using English names such as David or Emily, and others using ethnic minority names such as Nullah (Aboriginal), Zhiqiang (Chinese), Amit (Indian), Aphrodite (Greek), Mustapha (Arabic). An invitation to an interview was classified as a “success”.

The study found not only a distinct bias toward English names (29 percent success compared with 11 percent for all others), but also a distinct ranking of discrimination. Greek manes were comparatively successful (14 percent success), but all others – Aboriginal, Arabic, Indian and Chinese names – had success rates between 10 and 12 percent.

Unfortunately, as an academic study, it did not reveal the names or industries of the worst offenders.

There was evidence that some discrimination was explained by employers’ consideration of how customers might react to a person from a minority group. (“I’m not prejudiced but my customers are”.) There has been an extensive amount of work on the ethics of what are known as “reaction qualifications”. The general conclusion of ethicists is that such discrimination is not morally justifiable. There can be exceptions – a theatre company might justifiably argue that it cannot hire a “white” Othello – but such cases are rare.

Quite apart from the moral repugnance of such discrimination, it is plain dumb, because it involves the opportunity cost of unemployed or underemployed people who could be making more productive contributions to their employers and to the Australian economy.

3. Actually they were positions of authority. Leadership is a set of activities, it is not positional. ↩